Accounting Policies & Procedures: Meeting DOT Expectations

For government contractors working with state Departments of Transportation (DOTs), a well-documented accounting system is not just a best practice. It’s a requirement.

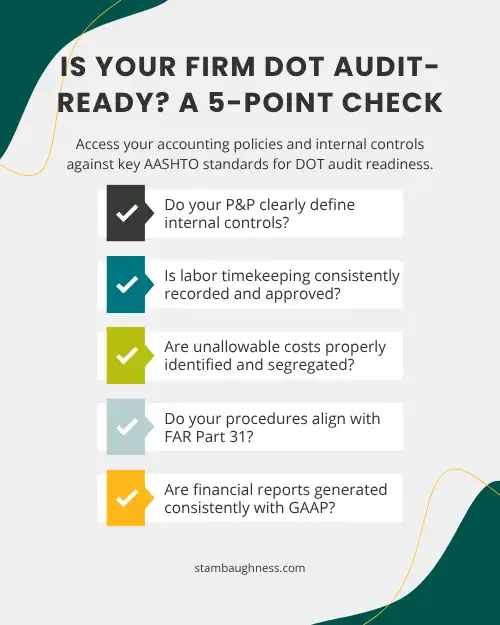

At the heart of every compliant accounting system are your Accounting Policies and Procedures (P&P). These documents are the first thing auditors look for when evaluating your firm’s readiness under the Federal Acquisition Regulation (FAR), Generally Accepted Accounting Principles (GAAP), and the AASHTO Uniform Audit & Accounting Guide.

Why Policies and Procedures Matter

Accounting policies and procedures are more than just paperwork; they are the blueprint for how your firm manages financial data, ensures compliance, and maintains internal controls. They serve three critical purposes:

- Say what you do – Document your policies and procedures in writing.

- Do what you say – Follow these procedures consistently in daily operations.

- Prove it – Maintain records and reports that demonstrate compliance.

Without written P&P, your firm may struggle to pass audits, defend cost allocations, or demonstrate the integrity of your accounting system.

Policies vs. Procedures vs. Work Instructions

Understanding the distinction between these terms is essential:

- Policies define the “what” and “why.” They explain your firm’s accounting principles, regulatory obligations, and internal control objectives.

- Procedures define the “how.” They describe the steps your team must follow to execute tasks in accordance with the policies.

- Work Instructions are the “click-by-click” guides, software-specific and often accompanied by screenshots, that support procedures but are not a substitute for them.

For example, your policy might state that all labor must be recorded daily and approved by a supervisor (FAR 31.201-6). The procedure would explain how employees complete timesheets and how supervisors review them. The work instruction would show how to enter time in your accounting software.

Audit Requirements for Written P&P

The AASHTO Audit Guide and the CPA Workpaper Review Program (Appendix A) both emphasize the importance of documented policies and procedures. Auditors are required to evaluate whether:

- The firm has written policies and procedures for key accounting functions.

- The procedures are consistent with FAR and GAAP.

- Internal controls are clearly defined and implemented.

- The firm’s practices match its documented procedures.

In fact, the Internal Control Questionnaire (ICQ), a required component of most DOT Audits, asks directly about the existence and adequacy of written P&P. If your firm cannot produce these documents, it may be flagged as high-risk, triggering additional scrutiny and disallowed costs.

What’s In Your ICQ: A Guide to Compliance

Discover how Internal Control Questionnaire (ICQ)disclosures impact your Indirect Cost Rate (ICR), align your written policies with actual accounting practices, and ensure FAR Part 31 compliance.

What Should Be Included in Your P&P?

While every firm is different, a strong accounting P&P manual typically includes:

- Revenue recognition and billing policies

- Timekeeping and labor distribution procedures

- Cost allocation methodology (direct vs. indirect)

- Treatment of unallowable costs (FAR 31.205)

- Payroll and fringe benefit accounting

- Purchasing and accounts payable controls

- Travel and expense reimbursement policies

- Month-end close and financial reporting procedures

- Internal control structure and segregation of duties

- Record retention and audit support protocols

These policies should be tailored to your firm’s size, structure, and accounting system, but they must align with FAR, GAAP, and AASHTO expectations.

Common Remediation Items

During audits, we often see firms flagged for:

- Missing or outdated policies

- Inconsistent procedures across departments

- Lack of internal control documentation

- No written treatment of unallowable costs

- Inadequate timekeeping or labor charging procedures

We strongly encourage firms to address these issues proactively, before they become audit findings. Based on our decades of work within the govcon space, we recommend two flexible solutions to help your firm establish or improve its accounting policies and procedures:

P&P Templates

Leveraging a professionally developed P&P template that includes common policies and procedures auditors expect to see is ideal for firms seeking a strong starting point. SN’s P&P templates meet the expectations of:

- FAR Part 31

- GAAP

- AASHTO Uniform Audit & Accounting Guide

We also include up to four (4) hours of consulting support to help you review, edit, and customize the content for your organization.

P&P Consulting Services

If you are a firm that already has policies and procedures in place but wants to refresh outdated documentation or identify areas to improve, consulting services are a great way to receive an expert review. Services for firms with existing documentation can provide:

- A compliance gap analysis

- Recommendations for improvement

- Guidance on internal controls

- Support for documenting cost treatment

Accelerate Your Compliance & Success

Your accounting policies and procedures are the foundation of your compliance program. They guide your team, support your accounting system, and demonstrate your firm’s commitment to integrity and transparency.

If you’re ready to strengthen your accounting foundation and accelerate your success in government contracting, let’s talk about how our P&P templates and consulting services can help your firm stay compliant, audit-ready, and confident in your accounting practices.