Why GAAP-Compliance Matters in GovCon Accounting

As government contract opportunities continue to grow for architecture, engineering, and consulting (AEC) firms, the pressure to meet federal compliance standards accelerates. One of the first hurdles many firms encounter is demonstrating a GAAP-compliant accounting system. This isn’t just a best practice; it’s a non-negotiable requirement for passing the SF 1408 Preaward Survey and securing flexibly priced contracts. Whether you’re new to government contracting or preparing for more complex awards, understanding Generally Accepted Accounting Principles (GAAP) is absolutely foundational to your Federal Acquisition Regulation (FAR) readiness.

What is GAAP?

GAAP stands for Generally Accepted Accounting Principles. Specifically, we’re focusing on U.S. GAAP for companies based and reporting in the United States. GAAP is a set of rules developed and maintained by the Financial Accounting Standards Board (FASB) to ensure that financial statements are complete, consistent, and comparable across different companies. It provides a standardized framework for the presentation of financial statements, with the FASB’s Accounting Standards Codification (ASC) serving as the single source of authoritative non-government U.S. GAAP.

When and Why GAAP Compliance is Required

While GAAP broadly applies to publicly traded companies and many private companies in the U.S., its relevance for government contractors is particularly pronounced. The U.S. Securities and Exchange Commission (SEC) requires publicly traded companies to file GAAP-compliant financial statements regularly. For private companies, GAAP compliance becomes essential when issuing financial statements outside the organization, particularly when these statements involve government contracts or other external reporting requirements. It’s important to note that the SF 1408 Preaward Survey of Prospective Contractor (Accounting System) explicitly requires GAAP compliance to achieve and maintain an adequate accounting system for government contracts. This foundational requirement ensures transparency and accountability for federal funds.

We often find clients contact us regarding GAAP compliance for three common reasons:

Loan Covenants

When obtaining new or increased financing, such as a line of credit or term loan, banks frequently require reviewed or audited GAAP-compliant financial statements as a loan covenant. While thresholds vary, we typically see this requirement emerge as debt facilities or loan values approach $5 million, though many lenders will accept internally prepared or externally compiled statements below that amount.

Regulatory Audits

As government contractors, your firm is subject to various regulatory audits, including FAR overhead audits, incurred costs proposal audits, and the SF 1408 survey (which, while technically a survey, functions as a critical assessment). All of these necessitate the adoption and adherence to GAAP as it applies to your firm.

Investor Relations

Whether you’re considering an internal ownership/leadership transition, a sale to outside parties, or a merger with another firm, investors – internal or external – will analyze your financial statements and expect them to be GAAP-compliant so they accurately compare with others in your industry and within their broader investment portfolios.

“As a government contracts lawyer, I hate to admit it, but to me, an experienced accountant is the most important professional for a government contractor. Robert is my go-to accountant when my clients bring me an issue involving government accounting, cost principles, audits, etc. He’s very good!”

The 10 Guiding Principles of GAAP

While not formally codified within FASB’s ASC, these ten basic principles clarify the primary mission of GAAP and outline what is expected of all who practice accounting. They form the essential foundation for reliable financial reporting.

- Principle of Regularity: Requires strict adherence to established rules and regulations.

- Principle of Consistency: Mandates the application of consistent standards throughout the financial reporting process.

- Principle of Sincerity: Emphasizes precision and transparency in all financial disclosures.

- Principle of Permanence of Methods: Upholds the long-term consistency in financial reporting methods.

- Principle of Non-Compensation: Requires reporting of both favorable and unfavorable financial situations without consideration of additional compensation.

- Principle of Prudence: Ensures that speculation does not influence financial work.

- Principle of Continuity: Assumes the organization’s operations will continue into the foreseeable future.

- Principle of Periodicity: Requires financial information to be reported in defined standard accounting periods, such as months, quarters, or years.

- Principle of Full Disclosure: Commits to disclosing the complete financial situation.

- Principle of Utmost Good Faith: Presumes honesty in all financial dealings and transactions.

Accrual vs. Cash Basis Accounting

The first fundamental GAAP requirement is maintaining accrual-based books. While cash basis accounting may be acceptable for tax purposes in many situations, it is not suitable for financial statements issued outside the organization, for effective internal management, or accurate industry benchmarking.

Accrual accounting recognizes revenue when it is earned and expenses when they are incurred, regardless of when cash is actually exchanged. This provides a more accurate picture of a firm’s financial performance over a period. In contrast, cash basis accounting focuses solely on when cash is received or paid out.

We often see smaller businesses maintaining “hybrid” books, recognizing some transactions on an accrual basis and others on a cash basis, sometimes aligning depreciation with tax returns. However, for GAAP compliance, a consistent accrual method is essential.

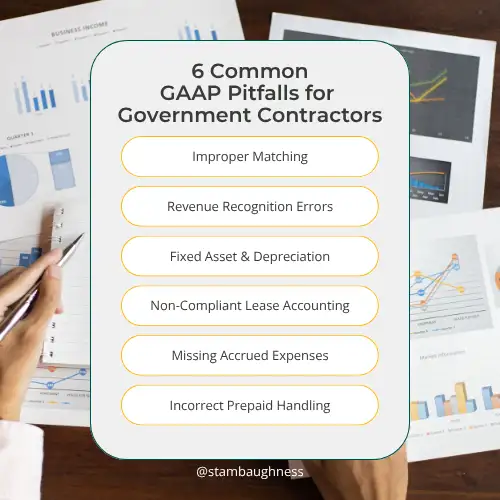

Common GAAP Issues for Small Firms

Matching

The matching principle aligns revenues with their corresponding expenses within the proper period. This means that revenue earned in April should have all related expenses also recorded in April. If your income statement shows extreme peaks and valleys in operating income, it’s a strong indicator that proper matching may not be occurring.

Revenue Recognition

Revenue Recognition is a complicated topic, worthy of a separate article. In summary, ASC 606 provides specific criteria to determine if revenue is earned at a point in time or over time. It’s important to note that recognized revenue does not necessarily equal billings; the proper revenue recognized may be higher or lower than the amount on a customer invoice.

Fixed Assets & Depreciation

A company’s fixed assets must be accurately listed on the balance sheet with their corresponding accumulated depreciation. Book depreciation, typically the straight-line method, results in more uniform expense recognition over an asset’s life. Tax depreciation, often accelerated by the government to induce spending and defer corporate income taxes, should not be recorded in your financial books for GAAP purposes.

Lease Accounting

ASC 842 requires companies to record their lease liabilities and related right-of-use (ROU) assets on the balance sheet. It also requires the lease expense to be recognized as a straight-line amortization of the present value of all outstanding payments. Many firms record the lease expense each month without reflecting the underlying asset and liability on the balance sheet. Fortunately, specialized software can greatly assist with this.

Accrued Payroll, PTO, & Expenses

Directly related to the matching principle, expenses are often recorded even before an invoice is received or cash changes hands. Some examples include equipment or supplies received without an invoice, time worked without a payroll run, and Paid Time Off (PTO) earned but not yet used. In each scenario, the company has incurred expenses and liabilities that must be captured to accurately represent the firm’s financial position in the proper period.

Prepaid Expenses

Also linked to matching, prepaid expenses (such as liability insurance paid for the entire year upfront) must be recorded as an asset on the balance sheet and then systematically amortized as an expense over the periods in which they benefit. Recording the entire expense in the month the check is written would distort the financial picture, overstating expenses in that initial period and understating them in future periods.

Accelerate Your Firm’s Federal Success

Architects, engineers, and consultants pursuing government contracts know that GAAP compliance is more than just an accounting practice; it’s a non-negotiable requirement. It’s also one of the core areas evaluated in SN’s FAR Readiness Assessments. If you’re unsure whether your current practices would pass a government audit, or you just want peace of mind, we can help. We’ll assist you in assessing your current processes, identifying any gaps, and getting fully FAR ready.

Partnering with Stambaugh Ness means your firm can confidently meet GAAP compliance requirements, enhance financial reporting accuracy, and strengthen credibility with government agencies and financial institutions.

Ready for peace of mind and sustained growth in the GovCon space? Connect with our team today!