Remote Work and State Tax: Navigating “Convenience” and Reciprocity

The rise of remote work has brought about significant changes in the way businesses operate. While this shift offers benefits like increased employee satisfaction and cost savings, it also presents new challenges, particularly when it comes to state and local tax laws. With employees working across state lines, understanding how state tax rules apply is more important than ever.

For businesses with remote workforces, two key concepts are essential for getting payroll reporting correct: the “convenience of the employer rule” and reciprocity agreements.

“Convenience of the Employer” Rule

The “convenience of the employer” rule can lead to complex reporting and tax situations. If an employee works remotely for their own convenience rather than for the employer’s, their wages may be taxed in the state where the employer is located, even if the employee never physically works there. This could result in double taxation – where the employee pays taxes to both their state of residence and the employer’s state.

For example, consider an architect living in Pennsylvania but working remotely for a firm based in New York. Even though the architect never traveled to New York, their wages could still be taxed by New York under the convenience rule. This can complicate reporting and tax compliance for both the employee and the firm.

Determining “Convenience”

The line between whether remote work is for the employer’s or the employee’s convenience can be unclear. Factors that may influence this include:

- Whether the firm provides a dedicated workspace at the office.

- Whether the employee is required to work remotely for business reasons (e.g., to oversee a project in another state).

- Whether the firm reimburses the employee for home office expenses.

Reciprocity Agreements

To avoid double taxation, many states have entered into reciprocity agreements. These agreements allow employees who live in one state but work in another to only pay tax on their wages to their state of residence.

For instance, if an engineer lives in Indiana and works for a firm in Michigan, the firm only needs to report wages and withhold state income taxes for Indiana, thanks to the reciprocity agreement between the two states. This simplifies reporting and tax compliance for businesses with remote/hybrid employees.

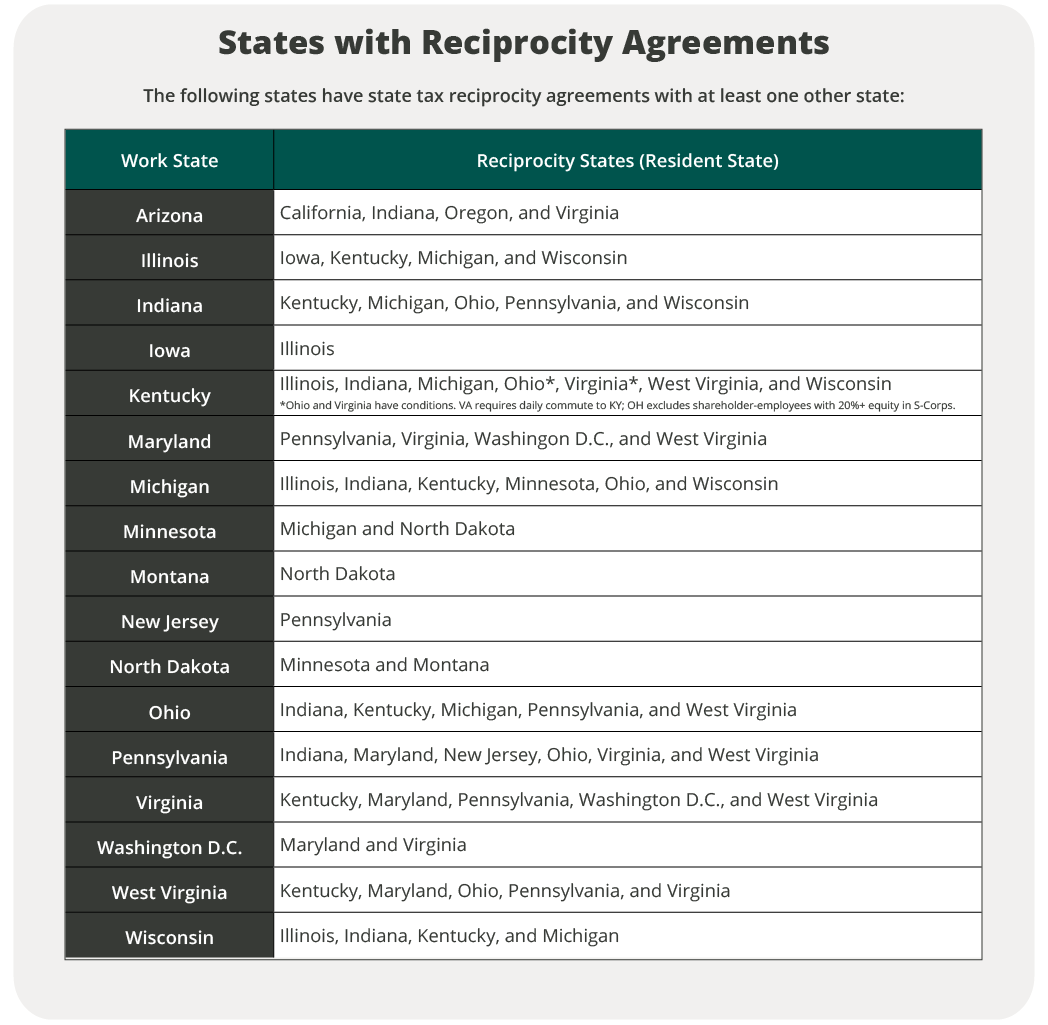

States with Reciprocity Agreements

Not all states have reciprocity agreements, so it’s important for businesses to be aware of which states have them. Employees who live in a state without a reciprocity agreement with their employer’s state may need to file taxes in both states. However, many states offer tax credits for taxes paid to other states, which can help reduce the tax burden.

Accelerating Success with Your Remote Workforce

The interplay between the “convenience of the employer” rule and reciprocity agreements can create a complex tax landscape for businesses with remote employees. To avoid compliance issues and reduce tax burdens, employers must stay informed about state taxes. A proactive approach to these multi-state challenges requires staying informed about state taxes. Consulting with a tax state advisory professional can help ensure proper withholding practices and mitigate risks for both the firm and its employees.

For a deeper dive into these tax complexities, including best practices for managing remote and traveling employees, watch our on-demand webinar, Remote & Traveling Employees: The Snowball Effect. Our state tax advisory experts explore compliance considerations and strategies for navigating multi-state payroll and reporting challenges.